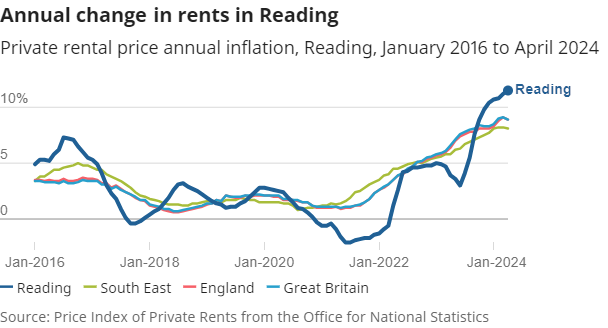

Over the past decade, the cost of renting in Reading has seen a significant upward trajectory, outpacing many other towns and cities in the Thames Valley.

According to the latest data from the Office for National Statistics (ONS), the average rent in Reading has increased by approximately 35% since 2014, highlighting the pressures faced by renters in the area.

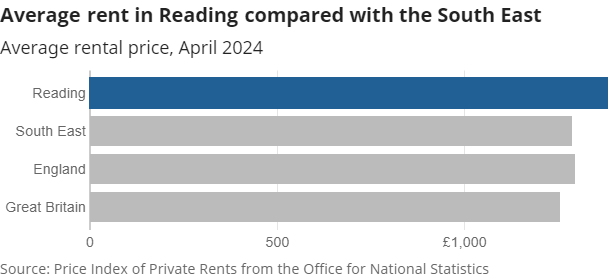

In 2014, the average monthly rent in Reading was around £850. Fast forward to 2024, and that figure has surged to £1,150. This increase is stark when compared to the average rental growth in the South East, which stands at around 25% over the same period. This makes Reading one of the most expensive places to rent in the Thames Valley region, surpassed only by Oxford and well ahead of the average for the South East of England.

Similar rises have been seen in other towns and cities in the Thames Valley. For instance, Slough has seen a rent increase of about 28%, with the average rent rising from £780 to £1,000. Maidenhead experienced a 30% rise, moving from £900 to £1,170. Meanwhile, Newbury saw a more modest increase of 22%, with rents moving from £750 to £915.

Rents have been rising whilst house prices have actually experienced a fall over the past year. According to the ONS, the average house price in Reading was £327,000 in March 2024, down 4.7% from March 2023. This was steeper than the fall in the South East (1.3%) over the same period.

At the newly completed Huntley Wharf development in central Reading, rents average £1,800 - £1,900 for a two bedroom flat, whilst the lowest cost properties available for a two bed private rental on Rightmove at the time of writing were £1,150 for Bexley Court in Southcote and £1,200 for Heritage Court in Castle Hill.

Reading's cheapest rental in Bexley Park

Reading's cheapest rental in Bexley Park

So, why do rents continue to rise whilst property prices are falling?

Several factors have contributed to the rising cost of rent in the town. Reading has continued to flourish as a major economic hub within the Thames Valley, attracting numerous tech companies, financial services firms and, more recently, pharma companies such as Sanofi. The resulting influx of high-income professionals has driven up demand for housing, thereby increasing rental prices.

Many of these workers are reasonably transient, working for multinational companies where they may be transferred elsewhere at any time, or working on short and medium term contracts. Often rent is part of their relocation package and Reading rents are still considerably less than those of major cities around the world.

There has been an undeniable knock-on effect from the introduction of the Elizabeth Line, adding Reading to the greater London tube network. Property and rental prices in Reading remain low compared to the capital, despite high transport and travel costs. With the majority of major developments located in the centre of the town around the station, there was always room for the price arbitrage between rent plus travel cost to narrow to that of living in London.

More than a thousand homes have been built in Reading in the past year - 1,021 homes and flats were completed in 2023/24, of which 224 (21 per cent) are designated affordable and more than 10,000 new units are in the planning and development pipeline.

Despite this, the supply of new housing has not kept pace with demand. The lack of suitable land is often quoted as a problem by the council and developers, with part of Reading not being capable of development due to flooding issues and proximity to local nuclear facilities (see our May edition).

Regulatory changes in the buy-to-let market, including increased stamp duty on second homes and changes to mortgage interest tax relief, have made it more expensive for landlords to operate. These costs have often been passed on to tenants in the form of higher rents. The Council is now proposing extending licensing to all operators of any property rented to more than one person – they currently regulate houses of multiple occupancy (HMOs), defined as a house or flat occupied by three or more people, who form two or more households and share amenities (such as bathrooms or kitchen). Currently over 1,400 houses are regulated under the scheme. The extension of this regime to properties with three or four occupants comes with a hefty licensing fee of nearly £1,000 which landlords may choose to pass on to tenants. The new scheme would total around 3,000 properties across the town. Proposals are explained in this video produced by RBC and you can have your say here.

There remains a major disparity between the cost of private and public rental.

The difference in price between private and public (social) rental properties can be quite significant. Public rental properties, which are typically provided by local councils or housing associations, are usually more affordable than private rentals. As of 2024, the average cost for a two-bedroom public rental property in Reading is approximately £600 to £700 per month. This is nearly half the cost of the private rental market. Not surprisingly there are over 5,000 names on the waiting list for public rental in the borough and the town’s homelessness situation is well documented.

Although it is difficult to get accurate information, it is estimated that 500 individuals are currently homeless in Reading with around 25-30 individuals regularly sleeping rough on the streets and several hundred households in temporary accommodation.

On the cusp of a General Election and potentially sweeping potential political changes, what does the future hold for renters in Reading?

Well, the reality is that even local Labour politicians admit that there is little they can do to change the current situation. Property has replaced shares and pensions as the main investment vehicle for many Brits, and even as they now eschew being private landlords, institutions are stepping in. Properties such as the massive Thames Quarter development by Reading Bridge were developed solely for rental.

No political party can risk a crash in the housing market. Likewise, increasing housing supply is also difficult. Labour’s big idea is to develop ‘the grey belt’ and building new towns. The residents of Arborfield Green may have views on this approach that has left them with few facilities in a massive housing development. This may result in increasing volumes of development, but the gap between public and private rental rates is a massive problem.

Labour's promise to build half a million new homes in its first five years in government (which it claims will be 'affordable') does not really signal much change from the 220,000 houses that were built in 2022 and 2023 and any intervention in the market is likely to see the major housing developers ‘land bank’ in the hope of reducing supply and protect the inflated prices they can charge for homes.

In addition, increased regulation around rental properties is likely to take more small landlords out of the market. After all, why put up with all the hassle of regulation and tenants and leaky roofs for a 4% return when you can get 5% in the bank?

Since the nineties the cost of rent as a percentage of an average Brit’s disposable income has risen from 20-25% to 40-45%. This has a significant impact on local economies and it is possible to see an almost direct correlation with the decline in local pubs, for example, as people have less disposable income.

Whoever comes into power in July 2024 has a seemingly insurmountable challenge on their hands.

https://www.ons.gov.uk/visualisations/housingpriceslocal/E06000038/#rent_price

Comments

No comments yet. Be the first to share your thoughts.

Join the conversation

Subscribe to inReading to leave a comment.